The BNPL Solution: Boost Your Order Values and Conversions in a Challenging Economy – Without the Risk of Payment Plans

You ever feel like your price is hurting sales?

Pricing your products and services is a tough game. On one hand, you don’t want to be the cheapest game in town. Cheap prices are synonymous with low quality. But on the other hand, higher prices means fewer customers.

It can feel like a “race to the bottom”. Every passing week, you feel more downward pressure to lower your prices in an attempt to convert some more buyers.

But lowering prices has its own consequences. When you make less from each customer, you have less margin for error as a brand. You have less money to invest back into finding new customers on ad platforms like Facebook or Google. Lower prices can mean you’re stuck as a “one man team”, with no extra cashflow to hire some help.

And to top it all off, lower prices obviously means you keep less profit at the end of the day.

What if there was a way to raise your prices, while converting more visitors into paying customers? A way to take your price, and re-frame it in the mind of your audience. How do we turn price from a major negative, into a major positive?

Well the answer rests on one simple word: flexibility.

Flexibility to meet your customers where they are. Inject choice into how you sell your digital products, and watch even your most expensive products fly off the digital shelves.

Let’s explore what “flexibility” means when talking about your eCommerce. And why now, more than ever, creators who are embracing flexibility in their payments are winning.

How A Recession Dampens Your eCommerce

65% of economists polled by Bloomberg expect the US to fall into a recession in 2023¹. The World Bank says the global economy is “perilously close to falling into recession.”²

Meanwhile, although we have not “officially” fallen into a recession, consumers across the world are feeling the pinch from persistently high inflation. And they’re cutting back on discretionary spending.

Bain & Co. found that almost 80% of US and European consumers are reducing or planning to reduce spending.³

US retail spending is pulling back, with major retailers noting that many shoppers are leaning towards value-driven brands.⁴

The personal savings rate of US consumers has plummeted back down to under 4%.⁵

And here’s the truth about your digital products, services, and courses:

No matter how helpful they are – or how much of a difference they can make in your customers’ lives – consumers will still tend to place these digital offerings firmly in the “non-essential spending” category.

This means that when the economy is gloomy and finances are tight, the decision to buy your product – instead of something else – becomes a lot more difficult.

And the worst part is:

Your High-Ticket Offerings – the Profit Center of Your Business – Will be Impacted the Most

Did you know that high-ticket products (those priced at $499 and above) make up only 5% of all of SamCart’s transactions – yet account for 55% of all revenue processed through our platform?

In short, 5% of our creators’ products are responsible for 55% of their revenue.

On the flipside, it also means that low-ticket offers make up 95% of their transactions – but only account for 45% of their revenue.

This makes high-ticket offers the “profit centers” for businesses like yours. These backend products are the lifeblood that feeds growth. When these offers are selling, you are able to scale your customer acquisition on the front-end…with more cash to reinvest into acquiring new customers through ad networks or hiring team members to handle-back office functions, so you can focus on developing your brand and next product to sell.

Yet, it is these profit centers that are the most impacted by the tighter economic conditions we face today.

When you’re asking someone to spend $500, $1,000, $2,000, or more with you in such an environment, there is an immense amount of friction. Those purchases are not made lightly. Your offerings are put under intense scrutiny, and the customer’s willingness to buy is much lower.

As conversions on your high-ticket offerings suffer, it can significantly damage your business economics. Without these highly profitable sales, your entire brand might be in hot water.

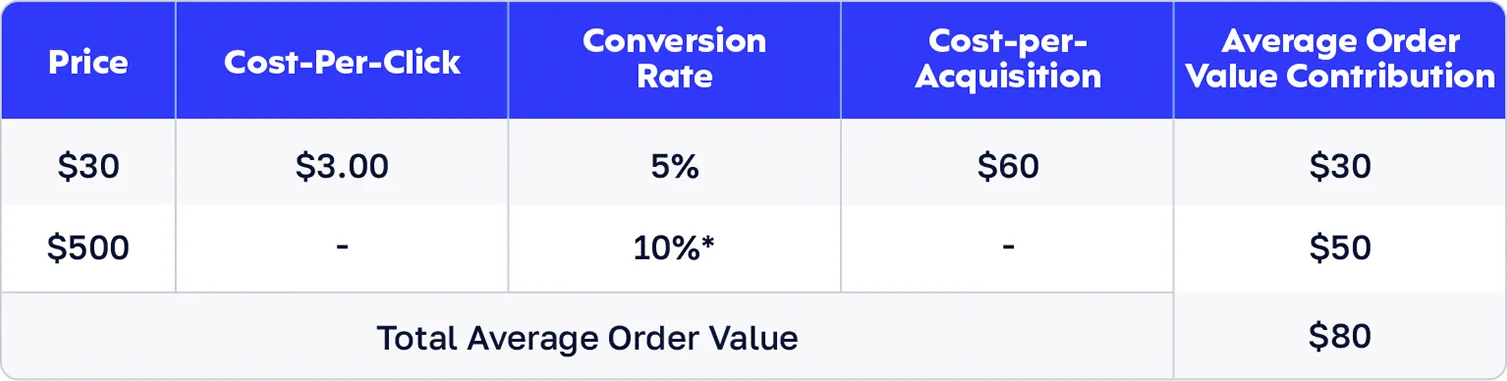

Let’s look at the example of a very common sales funnel; a $30 front-end offer with a $500 optional upsell. Let’s assume this is a real offer that is being marketed to cold traffic.

Base Scenario

In the base scenario, you can see that the funnel is profitable. It costs $60 to acquire a customer, with you getting an average of $80 from each customer on their first order. There’s a healthy profit margin that justifies investing more to acquire more customers.

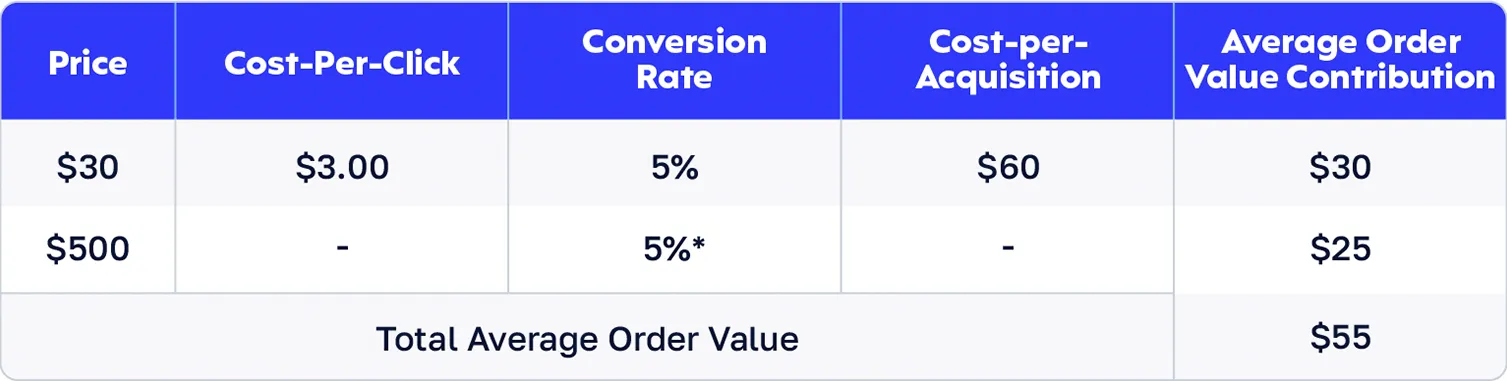

Recession Scenario

In the recession scenario, the only thing that changed was the conversion rate on the high-ticket upsell. The front-end conversion rate and cost-per-click stayed the same.

Yet, this sales funnel has become unprofitable… and that’s before accounting for other business expenses. If this math equation is not fixed, this business won’t be able to sustain itself for long. The math does not justify investing further.

So, the question is:

How can you make it easier for customers to buy your high-ticket offers in today’s challenging economic environment?

Most usually try a combination of the following 3 options:

Option 1: Cutting prices to boost conversions

This option is easy to understand. Lower prices stimulate demand. Yes, doing this will most likely increase your conversions.

But that does not happen in a vacuum. Slashing prices also slashes your Average Order Value. Any decrease in AOV could potentially cancel out the increase in conversion – lowering your overall profits.

Option 2: Making bigger claims in your copy and messaging

Another option is to compete on claims – making them more aggressive, with bigger and bolder promises. A better sales pitch can convince more visitors to take action.

But that runs the risk of overpromising and under-delivering… which could increase your refund rates, create dissatisfied customers, and impact your reputation. And if you’re in a niche with more regulatory requirements, you could even risk running afoul of the FTC and incurring legal penalties.

Overpromising could help acquire more customers. But it is unlikely to make a meaningful change in the long-term viability of your brand.

Option 3: Changing the payment terms to lower the initial cost

This is when you take a high up-front cost, and break it into smaller chunks paid out over time. This strategy can also be referred to as offering a “payment plan.” SamCart’s database proves that adding a payment plan to your checkout flow increases conversion rate by +17%.

However, using payment plans carries its own risk. If your customer mix leans too heavily in favor of buying payment plans, you can destroy your lifetime customer value (LTV) and profit margins thanks to the dreaded “C-word” – churn.

Churn is the rate customers cancel their service. If churn was 10%, that would mean that every 30 days, one in ten customers are ending their relationship with your brand. Churn is the silent killer for any business with recurring revenue.

Because the truth is, not all buyers complete their payment plans. A lot of times, customers make the first payment and receive all the materials, quickly digest as many learnings as they can, decide they’ve gotten all the benefits, and stop making any of the remaining payments.

In fact, SamCart’s database proves that the average payment plan only survives 4.33 months.

It is such a well-known issue that one of the most frequent points of discussion among high-ticket offer owners is how to reduce the number of customers who abandon their payment plans halfway.

The worst part is – there’s often no legal recourse available (or it’s just not worth pursuing). You’ll have to bear the full risk of the customer “defaulting” on their payment plans.

That’s why the total amount of payment plan installments is usually significantly higher (anywhere from 10 – 50% more) than the “pay in full” payment – to mitigate the additional risk. And it’s also why you see digital creators try tactics like⁶

Sending customers a whole new course for free after they’ve completed a certain number of payments, so customers are incentivized to continue paying.

Presenting the payment plan option first – only then followed by a “pay in full” option with a lower overall price tag – just to psychologically incentivize buyers to pay in full.

Offering additional bonuses for customers who choose to pay in full instead of taking a payment plan.

Payment plans can be such a headache that many creators only feel they’re worth it if it’s for an offer with some sort of recurring function – like ongoing membership or coaching – to act as a natural incentive for the customer to complete the payment plan.

But the good news is there’s a fourth option available:

An option that allows you to offer your customers a frictionless way of instantly lightening the price load – without requiring you to bear any default risk whatsoever.

What if there was a way in which your customer receives many of the same benefits of a payment plan without having to pay a higher total price…

While you get the full payment upfront without having to worry about your customer “defaulting” on the payment plan?

And to top it off, what if you could use this option not just on your higher-ticket offers, but on your lower-priced products as well?

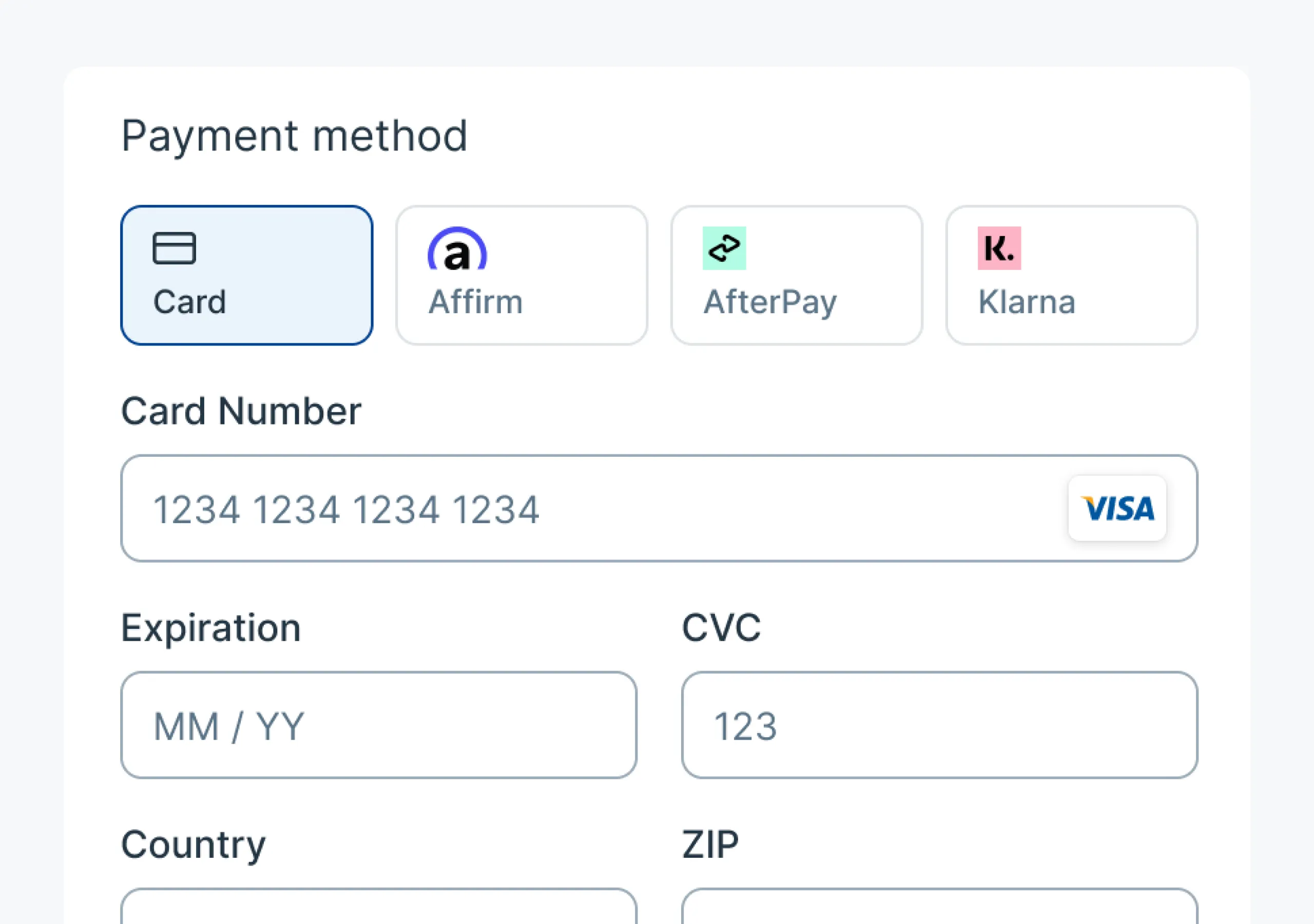

Introducing Buy Now Pay Later (BNPL) Options From SamCart

If you haven’t heard of Buy Now, Pay Later (i.e “BNPL”), here’s what you need to know:

BNPL is a payment option that allows customers to split the cost of their order into smaller, interest-free payments over time.

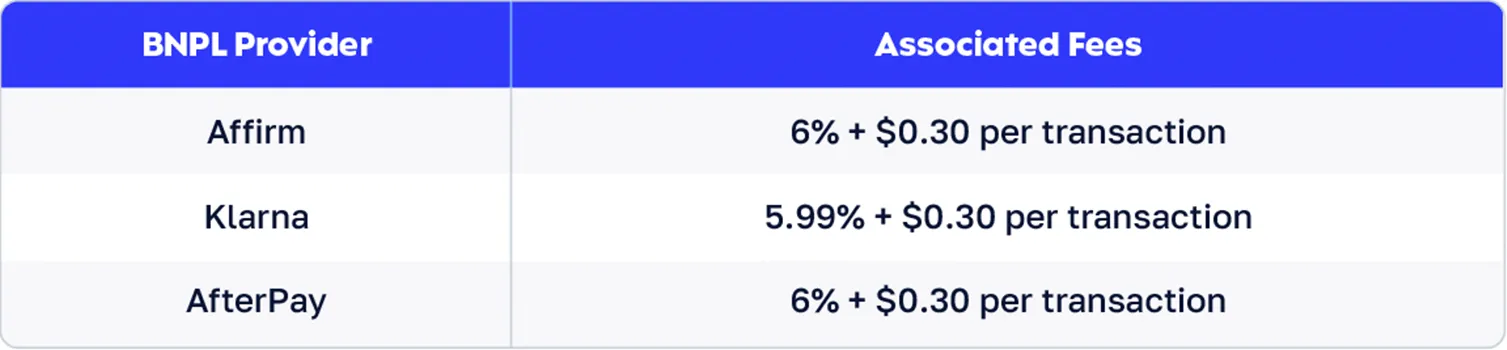

BNPL services are offered by major third-party companies – such as Affirm, Klarna, and AfterPay – that take on all the underwriting and associated repayment risk (including collections) so that you as a digital seller don’t have to worry about anything else.

For customers, using BNPL is extremely easy as it’s usually already built into the seller’s checkout page.

Online sellers will receive the full payment upfront – minus the 6% transaction fee charged by the BNPL provider.

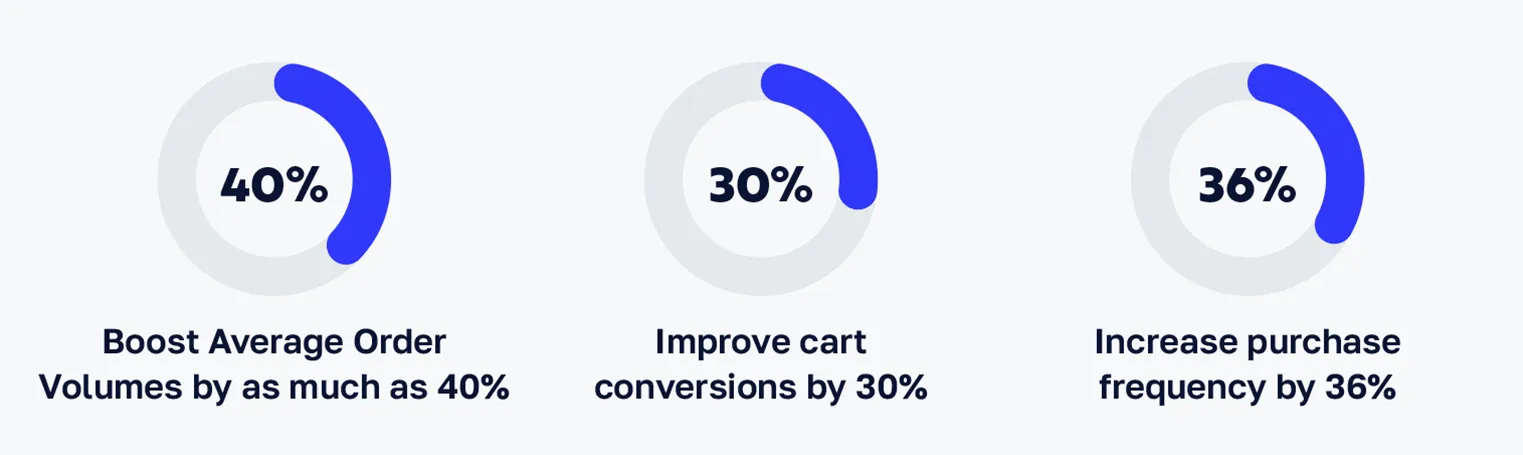

Research by the major BNPL providers have found that using BNPL services can help businesses⁷:

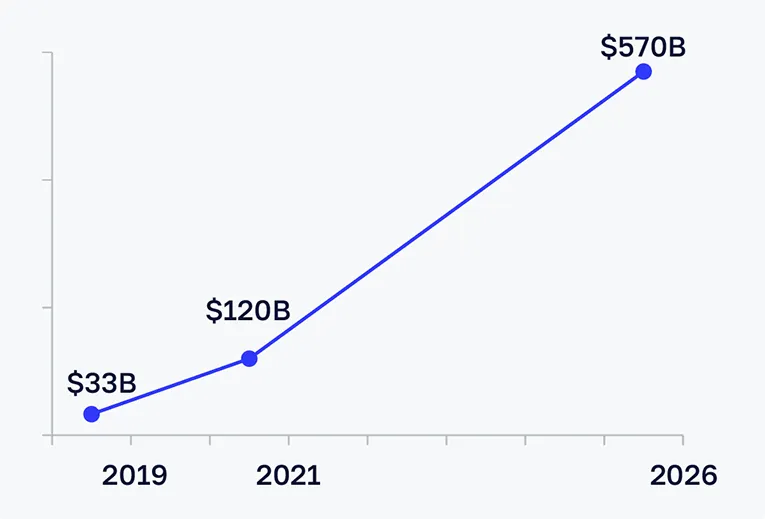

With stats like these, it’s no surprise that BNPL transaction volumes have been rapidly accelerating. Between 2019 and 2021, total BNPL transaction volumes surged from $33 billion to $120 billion – a nearly 400% increase⁸. By 2026, that number is expected to hit $570 billion.⁹

And after getting dozens of requests on our Product Board (see sidebar), we decided to launch a beta test to see the effect of BNPL checkout options in the online creator space.

The beta test results revealed that BNPL may be even more beneficial for digital creators compared to the broader online business space.

For example, one beta test online seller operating in the real estate niche discovered that 13% of their transactions for products in the $500 – $1,000 range were being made via BNPL. By comparison, the broader BNPL transaction market share is about 5%.¹⁰

This means that digital product buyers might be over 200% more likely to be willing to use BNPL options.

The only fees associated with BNPL transactions are those charged by the BNPL providers themselves.

But while these fees do create an additional cost on your part:

3 Reasons Why Every Creator Needs To Offer Buy Now, Pay Later

Reason 1: You get paid in full, right away.

When a customer purchases with Buy Now, Pay Later options, you (the seller) get paid right now. Customers will work out a payment plan that fits their budget. But your customers aren’t paying you each month. They are paying BNPL providers.

No need to worry about your customers reneging on their payment plan obligations

No need to waste your customer support resources chasing these customers

And no need to alter your product to spread out the benefits over the duration of the payment plan

As the math below shows, it’s likely more than worth it.

Say you have a $997 product that also has a payment plan of four equal payments of $297 each. Here’s how much revenue you’ll get per 100 sales for both options.

BNPL

Payment Plan

*Note that completion rates are based on the previous payment i.e. an 80% completion rate for Payment 3 means 80% of customers who made Payment 2 also made Payment 3.

As you can see, even with optimistic payment plan completion rates, you still get more revenue using BNPL despite the slightly higher processing fees.

Further, this assumes an equal number of customers for both the BNPL and payment plan. It does not account for any increase in conversion rates and Average Order Values that would likely result from offering BNPL payment options.

Reason 2: Your Customers Are Very Likely To Spend More

Since BNPL fees are about 6%, all it takes is a 6.4% increase in your average order value for it to fully compensate for the additional fees. When your customers spend more, your profits explode.

Research has shown that BNPL payment options could increase your Average Order Values by up to 40% across the board. We’ve even seen reports of online creators seeing AOV boosts by as much as 75%¹¹, including by some members of SamCart’s BNPL beta customer group.

Reason 3: BNPL works with cheaper products, too

It’s usually only worth offering payment plans on products in the $500 price range or higher. Yet, you can even offer BNPL payment options on your lower-priced products. In fact, only Affirm has a minimum order value, which is only $50.

It’s usually only worth offering payment plans on products in the $500 price range or higher. Yet, you can even offer BNPL payment options on your lower-priced products. In fact, only Affirm has a minimum order value, which is only $50.

List of non-U.S. countries supported by our BNPL providers:

Austria, Belgium, Denmark, Estonia, Finland, France, Germany, Greece, Ireland, Italy, Latvia, Lithuania, Netherlands, Norway, Slovakia, Slovenia, Spain, Sweden, Canada, United Kingdom, Australia, New Zealand, Spain

BNPL Gives You A Competitive Advantage

The benefits of BNPL payment options are simply too great to ignore – especially as the economic environment becomes more challenging.

As such, we’ve decided to integrate BNPL checkout options – provided by Affirm, Klarna, and AfterPay – into SamPay.

As of April 19, 2023, BNPL checkout is now automatically enabled for all SamPay users.

You can choose to switch it off in your Stripe dashboard if you want. But you do not have to do anything to offer BNPL checkout – it’s already been fully integrated into SamPay and is available on nearly all of SamCart’s checkout page layouts.

² https://www.bbc.com/news/business-64213830

³ https://www.bain.com/insights/as-costs-rise-consumers-tighten-their-belts-infographic/

⁵ https://www.wsj.com/articles/consumer-spending-inflation-economy-11675093472

⁶ Taken from Facebook group of online course creators and marketers

⁹ https://www.statista.com/statistics/1311122/global-bnpl-market-value-forecast/

¹⁰ https://www.statista.com/topics/8107/buy-now-pay-later-bnpl/#topicOverview

¹¹ Taken from Facebook group of online course creators and marketers